The Leatherback Long/Short Alternative Yield ETF (LBAY) (the “Fund”) net asset value (NAV) declined by 1.44% in September, compared to a decline of 4.77% for the S&P 500 Index. LBAY paid its thirty-fourth consecutive monthly distribution, at $0.075 per share in September. This is a 2.31% SEC yield versus the S&P 500 Index dividend yield of approximately 1.61%, and the 10-Year US Treasury yield of 4.572%. Year to date as of September 30, 2023, NAV for the Fund has declined 9.97%, compared to an advance of 13.07% for the S&P 500 Index. NAV performance for the Fund to date since inception (November 16, 2020) has produced a 40.74% cumulative total return and a 12.64% annualized total return.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling (833) 417-0090. The gross expense ratio for the fund is 1.32%.

View LBAY standardized performance here.

The Fund’s NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the Fund was traded.

FOR LONGER OR FOREVER

For well over a decade, US interest rates remained ultra-low. This created what many now view as an ideal environment for risk-taking. “Lower for longer” was the investing mantra from around 2008 through 2022. Government bonds and the safest fixed income instruments yielded next to nothing, while long duration* equities outperformed broad markets. In response to rampant global inflation, policymakers mandated an end to the party, and rates began to ratchet higher throughout the last year and a half.

“Inflation is like toothpaste. Once it’s out, you can hardly get it back in again. So the best thing is not to squeeze too hard on the tube.” — Dr. Karl Otto Pöhl

Market participants have been predicting inflation has peaked and that the worst may be behind us. As a result, we suppose an overoptimistic hope for rate cuts has sparked the US equity rally during the first half of 2023. As previously entrenched expectations are reluctantly reset and investors continue to digest the current market environment, we believe that long-term interest rates are sticky and are going to be here for a while. Given this, we think it is likely that equity market multiples will compress, and companies we find overvalued may suffer the consequences. Allocators may no longer need “bond proxy” equities, as bonds now maintain positive real yields. It is our thought that shareholder yield is likely to drive total return for equity investments. In our opinion, companies that are unprofitable and appear to require perpetual cheap capital are attractive short candidates. Finally, we envision absolute return long/short strategies are likely to outperform levered long* private and public equity investments.

BACK TO THE FUTURE

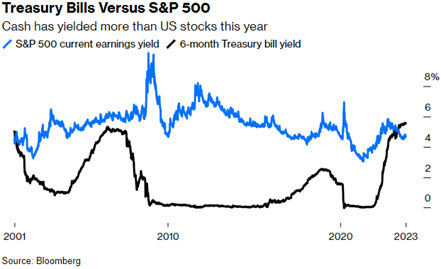

We are revisiting times that a good portion of current investors have either never experienced or may seem too long ago to remember. It may also be a bit of a shock for savers that their money is finally yielding something tangible. “For the first time this century, cash pays a higher yield in interest than the S&P 500 does in earnings — and with cash you actually get the cold hard money in your hands, rather than relying on accountants to calculate corporate profits correctly.”3 We find the below visual impressive:

In an insight earlier this year, we discussed the concept of the magical 5% number on interest rates, and how this may sometimes be thought of as a psychological level for investors lending their cash at a perceived “attractive” rate. Shorter-term interest rates have seen this level for several months now, but interestingly the 10-year Treasury briefly touched the 5% yield level during the fourth week of October. It hasn’t breached this rate since 2007. The staggering speed with which interest rates have risen this year has likely introduced a level of volatility to the fixed-income world that few were expecting.

“Five percent is more or less the average of investment-grade rates since the time of Alexander Hamilton…The problem is the structures that 10 years of ultra-easy money brought about. People blame it on the normalization of rates. The previous bout of abnormal rates is the problem.”4 - James Grant, founder and editor of Grant’s Interest Rate Observer.

PORTFOLIO REVIEW5*

In our opinion, a new normalized environment of higher for longer interest rates is constructive for active management and fundamental long/short strategies. We believe shareholder yield, which is core to our strategy, will drive future total returns as stock multiple expansion could be more difficult to achieve. Our current portfolio reflects many long positions with what we think are below market multiples, healthy growth profiles and appealing shareholder yield. We highlight one current long position, Old Republic International Corporation (ORI), a $7.7B market cap specialty insurer that currently maintains a 3.6% dividend yield and has repurchased $756mn of its own stock (nearly 10%) since the 3rd quarter of 2022. We feel the company maintains a conservative, liquid investment portfolio and a newer management team that seems constructive with capital allocation. The company currently trades for a forward price to earnings multiple* of around 10x, has increased its dividend for 42 consecutive years, and we believe the company could be an attractive takeout candidate.

Next, we view the setup on the short side of the ledger as increasingly interesting. We are looking for unprofitable companies that have perpetually relied on easy access to cheap capital. Additionally, we continue to favor the consumer discretionary sector shorts thesis. As we have outlined in previous writings, we think the difficulty experienced by consumers to maintain elevated levels of spending is just getting started, as the consumer credit environment continues to evolve.

View LBAY top 10 holdings here. Holdings are subject to change. Characteristics and metrics of the companies shown are for the underlying securities in the fund’s portfolio and do not represent or predict the performance of the fund. There is no guarantee that a company will pay or continually increase its dividend.

FINAL THOUGHTS

We hope our investor partners enjoy our monthly perspectives. We are finding many compelling ideas both long and short and we look forward to continuing our dialogue in the weeks and months ahead.