The Leatherback Long/Short Alternative Yield ETF (LBAY) (the “Fund”) net asset value (NAV) declined by 2.44% in August, compared to a decline of 1.59% for the S&P 500 Index. LBAY paid its thirty-third consecutive monthly distribution, at $0.075 per share in August. This is a 2.06% SEC yield versus the S&P 500 Index dividend yield of approximately 1.54%, and the 10-Year US Treasury yield of 4.109%. Year to date as of August 31, 2023, NAV for the Fund has declined 8.66%, compared to an advance of 18.73% for the S&P 500 Index. NAV performance for the Fund to date since inception (November 16, 2020) has produced a 42.79% cumulative total return and a 13.62% annualized total return.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling (833) 417-0090. The gross expense ratio for the fund is 1.32%.

View LBAY standardized performance here.

The Fund’s NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the Fund was traded.

JUST IN CASE

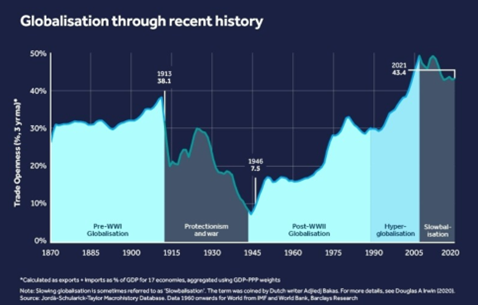

Over the past several decades, the world progressively “shrank”. Companies of all shapes and sizes, and more broadly, economies at large expedited a shift in scope from the full business cycle operating locally to a tilt toward an international scale. The phenomenon of globalization was here, and if you didn’t embrace it, you may as well have gotten out of the way. The view was if you didn’t get on board, you were in essence deciding to go out of business. Outsourcing and offshoring were terms popping up across many industries, and soon became ingrained corporate speak. This was a euphemism for firing part of the domestic workforce and sending jobs across borders. Just-in-time inventory became the rule to strive for, rather than the exception. This is the practice of keeping just enough inventory of items, or inputs to a product, on hand that are needed to fulfill orders ready to go out the door or when required for manufacture. Technological advances that we now take for granted made everyday occurrences out of what not long before seemed like impossibilities. The speed of communication, automation improvements, reduction in costs and delivery efficiency created an interconnected web on a macro scale. Global companies benefitted as corporate margins expanded while labor and manufacturing costs contracted.

The pandemic, which defined the start of the 2020’s decade, may have opened a Pandoras box and exposed how our global interconnectedness progressed to over-reliance on specific partners or locales. It becomes even more complex as we see trends emerge given varying degrees of nationalism and geopolitical protectionism. Most consumers are familiar with supply chain issues, which is where a good bit of the inflation blame is being placed. As companies and service providers have realized just-in-time inventory caused shortages, inefficiencies, and cost increases, many have switched to procuring larger amounts of inventory in an attempt to alleviate past supply headaches. Inventory is being managed at levels, “just in case.”

This implores the question: Is this experiment still working?

A RETURN TO SENDER

It is interesting to us that we appear to be in the midst of a shift back from “the hyper-globalization period from 1990 to 2008… to a period of relatively stagnant ‘slowbalisation’, [which] appears to be moving towards deglobalisation3.”

This could be an example: Maybe it started with the Sales team moving away from the Design, Engineering, and Manufacturing teams to a new location within a building. From there, maybe Design and Engineering moved to a separate building. It’s possible Engineering was then moved to a separate domestic city due to lower employment cost and real estate values. Finally, perhaps Manufacturing was outsourced (fired locally) and sent overseas to be replaced by workers distant from the location of the core business. The thought then might have been, if it seemed to work for Manufacturing, then maybe Engineering would be next. The question we wonder is how does the saving in immediately observed overhead cost compare with the negative intangible costs?

Has this global interconnectedness of business operations caused a disconnect with core business success? Are companies becoming siloed, and do all segments understand the business they are in? Do outsourced or offshored constituents share the vision, accountability, and ownership style of the company? Has the connection to the customer, both internal and external, been compromised? Are geopolitics impacting supply or demand? We may be starting to see companies and industries acknowledge this, as they now realize that some of these intangibles have been exposed as unintended costs that can now be tangibly observed over the longer time period. We are beginning to hear the term onshoring, albeit minimal, and a recognition that costs that have become tangible may be curtailed by returning jobs domestically that were sent overseas. With the world now reversing into potential deglobalization, we wonder if this additional domestic investment will lead to contracting margins and slower growth. It may not take us too long to find out.

PORTFOLIO REVIEW4

Since peaking at the end of July, the S&P 500 Index has struggled over the last several weeks. The narrow market leadership seems exhausted, with many names that far outperformed the market through the first seven months of the year rolling over. Meanwhile, interest rates have been grinding higher globally. We believe interest rates will be higher for quite some time. We continue to maintain short positions in several real estate investment trusts (REITs) which tend to inversely perform when compared with the direction of interest rates. We maintain shorts in legacy data center REITs Digital Realty Trust, Inc. (DLR) and Equinix, Inc. (EQIX) as well as industrial warehouse REIT Prologis, Inc. (PLD).

This month we want to highlight our short position in Planet Fitness, Inc. (PLNT). Interestingly, PLNT’s 50-year-old CEO was fired abruptly in mid-September. This follows a very brief tenure of its President, who resigned after just 5 months on the job at the end of May. For those that can recall, we highlighted PLNT as a short early last year, noting that its business practices may be suspect and aggressive. We think there may be more bad news to come, and we currently maintain our short position.

View LBAY top 10 holdings here. Holdings are subject to change. Characteristics and metrics of the companies shown are for the underlying securities in the fund’s portfolio and do not represent or predict the performance of the fund. There is no guarantee that a company will pay or continually increase its dividend.

FINAL THOUGHTS

We hope our investor partners enjoy our monthly perspectives. We are finding many compelling ideas both long and short and we look forward to continuing our dialogue in the weeks and months ahead.