The Leatherback Long/Short Alternative Yield ETF (LBAY) (the “Fund”) net asset value (NAV) advanced by 5.84% in May, compared to 0.18% for the S&P 500 Index. LBAY paid our eighteenth consecutive monthly distribution, at $0.065 per share in May. This is a 2.54% SEC yield versus the S&P 500 Index dividend yield of approximately 1.53%, and the 10-Year US Treasury yield of 2.847%. Year to date as of May 31, 2022, NAV for the Fund has returned 19.54%, compared to a decline of 12.76% for the S&P 500 Index. NAV performance for the Fund to date since inception (November 16, 2020) has produced a 52.69% cumulative total return and a 31.7% annualized total return.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling (833) 417-0090. The gross expense ratio for the fund is 1.43%.

View LBAY standardized performance here.

The Fund’s NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the Fund was traded.

IT WAS ON THE TABLE

Don’t fight the Fed is the mantra that investors have been trained to use for years; the US Federal Reserve Board (the Fed) easy money policies provided market participants the backdrop to be long risk assets. Most recently, the Fed printed trillions of dollars to bail us out of the pandemic. In our opinion, there is little doubt that this money printing has led to excessive valuations in stock and bond markets and caused the highest levels of inflation in the US in forty years.

We think investors should remain true to the mantra and not fight the Fed. The Fed will be raising rates, and that is not the best environment for risk taking. The Fed’s response to the latest inflation numbers indicates policymakers may be more reactive than in control.

"A 75 basis point* increase is not something the committee is actively considering." – Jerome Powell on May 4, 2022

As it turns out, the 75 basis point* hike actually was on the table. The two-year US Treasury yield gapped higher by nearly a full percentage point in the span of a few short weeks. We are now starting to hear the word 4% being spoken by market experts as a potential interest rate level to be hit for multiple maturity levels. It was less than six months ago when the concept of breaching 2% was up for debate. Meanwhile, equity markets continue a painful re-rating, and consumer/producer prices continue the move into the stratosphere. We asked the question last month, and are doing so again: “…Is there anywhere to hide?” It’s becoming clear that price discovery is returning to markets. We view current market dynamics as healthy long-term, but we expect significant volatility in the nearer term as market participants and economic academicians assess the fluid macro backdrop.

“I think I was wrong then about the path that inflation would take. As I mentioned, there have been unanticipated and large shocks to the economy…. that I, at the time, didn’t fully understand.” – Janet Yellen

HAPPY TO PAY YOU NEXT TUESDAY

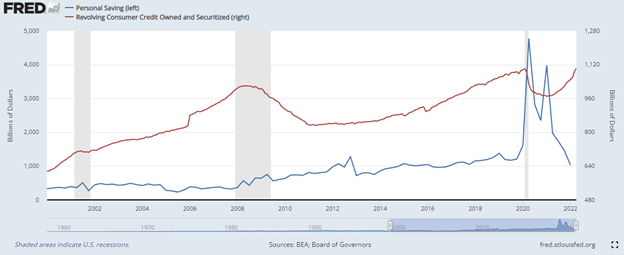

US personal consumption is the engine that drives the US economy, accounting for almost 70% of US gross domestic product. Notably, the amount of consumer savings has collapsed, while credit card and other revolver lines have hit all-time highs. We first pointed this out in August of 2021, and wondered if an uptick in credit borrowing was the result of rising costs and/or a potential savings depletion, or was it simply the resumption of past behaviors? We think the answer is obvious when seen in the below chart3, and likely has policymakers shuddering at all levels.

We think consumers are tapping credit lines to fund their lifestyles. Gas prices continue their step-up, and almost every household item has inflated higher. Consumers likely are anxious to “get out” again this summer, as the scars of being couped up during the pandemic remain. Exactly as consumers tap credit lines, interest rates are gapping higher; we question the medium-term ramifications for the US Consumer as we enter the second half of 2022 and then into 2023. A US recession is a real possibility.

WHO'S SWIMMING NAKED?

“Only when the tide goes out do you discover who’s been swimming naked.” – Warren Buffett

Will the triple whammy of depleted savings, higher debt levels, and the increasing cost of borrowing be too much and impair consumers? The next earnings cycle will be of great interest to us. We think the picture will become clearer on if and how businesses have been able to thread the needle of passing through costs to maintain margins, while at the same time attempting to retain those much-needed spenders. The pending riddle is how much is too much, and at what point do customers throw in the towel and simply say they can do without some of those items and services that are causing the trajectory seen the lines in the graph above? We think the next 18 months will provide the clarity around this question.

PORTFOLIO UPDATE*4

We recently initiated a short position in Doordash Inc (DASH). DASH introduced itself to public shareholders on December 8, 2020, issuing 33 million shares at $102 and raising $3.36 billion in proceeds. DASH’s business is local food delivery utilizing its Marketplace and Platform services “to grow and empower local economies”. In our opinion, DASH is an overvalued unprofitable technology stock that has limited ability to ever maintain sustained profitability. Notably, the only quarter in the company’s history when it turned a profit was in the second quarter of 2020, at the height of the COVID shutdown. Since then, the company has racked up seven consecutive quarters of losses and Wall Street forecasts are calling for further losses into the foreseeable future. At today’s levels, the company maintains a greater than $24.5B market cap, or over $21B enterprise value (EV) after netting its cash that’s left from its initial public offering. This equates to around a 3.4x EV/Sales multiple based on $6.1B in expected 2022 revenues. DASH’s closest peer GrubHub sold to Just Eat Takeaway.com in the Netherlands for over $7.3B in June of 2021. According to press reports, Just Eat Takeaway is shopping GrubHub for possibly as little as $1.3B and plans to offload the business less than a year after acquiring it. Other comparisons like UBER trade for less than 2x forward EV/Sales. We expect DASH to re-rate lower as more losses are likely reported in subsequent future quarters and years.

While we maintain a cautious view on the US macro-economic picture for the rest of 2022 and 2023, we note that the market is presenting some interesting values. Here we show our largest five long positions and their current market multiples, all of which we view as attractively valued.

View LBAY top 10 holdings here. Holdings are subject to change. Characteristics and metrics of the companies shown are for the underlying securities in the fund’s portfolio and do not represent or predict the performance of the fund. There is no guarantee that a company will pay or continually increase its dividend.

FINAL THOUGHTS

We hope our investor partners have enjoyed our monthly perspectives. We are finding many compelling ideas both long and short and we look forward to continuing our dialogue in the weeks and months ahead.