The Leatherback Long/Short Alternative Yield ETF (LBAY) (the “Fund”) NAV declined by 4.07% in November, compared to a decline of 0.69% for the S&P 500 Index. LBAY paid our twelfth consecutive monthly distribution, with an increase from $0.06 to $0.065 per share this month to celebrate the first anniversary of the Fund! This is a 3.57% SEC yield versus the S&P 500 Index dividend yield of approximately 1.32%, and the 10-Year US Treasury yield of approximately 1.45%. Year to date as of November 30, 2021, NAV for the fund has returned 11.08%, compared to 23.18% for the S&P 500 Index. Cumulative since inception (November 16, 2020) performance to date, NAV for the Fund has produced a 15.93% total return.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling (833) 417-0090. The gross expense ratio for the fund is 1.09%.

View LBAY standardized performance here.

The Fund’s NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the Fund was traded.

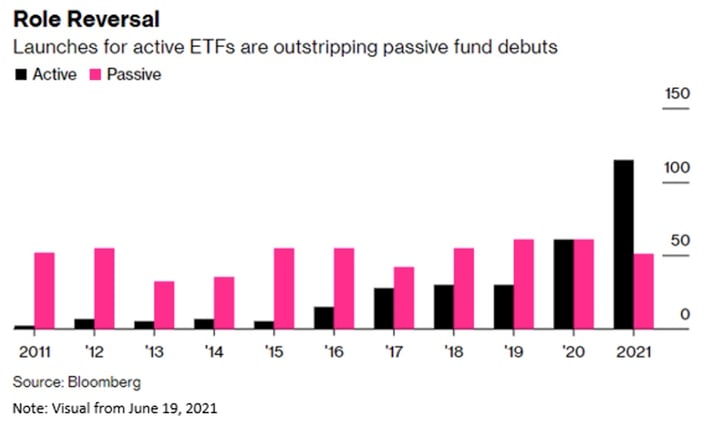

Since forming in 2020, the Leatherback mission has been to provide premier actively managed* alternative strategies to all investors in the most optimal, and potentially tax-efficient** way – which we think is the ETF wrapper. Metaphorically speaking, we think actively managed strategies delivered via an ETF has similarities to the advent of music videos taking over the music radio genre. Anyone remember the song and first music video ever from 1981? Well, in 2021, we think the ETF killed the mutual fund star!

As seen in the above visual3, we think our industry thesis is proving correct as ETFs gather record assets and are being led by active strategies. Legacy mutual fund managers initially were slow to evolve and are now rushing to convert mutual funds to ETFs. We think the ETF wrapper has been well-received due to its client-centric features, daily transparency, and potential tax-efficiency**. Paramount to our approach, we formed Leatherback to launch liquid alternatives utilizing ETFs, which we view as the most investor-friendly format available in the marketplace.

WHY INVEST IN LBAY?

• Capital Appreciation Potential - Targets a net long exposure of between 75-110% invested across high shareholder yielding and income producing securities

• Targeted Monthly Distributions - Seeks to generate a monthly payout through dividends, interest and covered option writing

• Long/Short Strategy with Full Transparency - Daily disclosure of all long and short positions

• Less Correlation to Equity Markets - Seeks downside protection by taking short positions in overvalued securities

• Cost Effective - Offers a lower cost option to liquid alternative mutual funds and long/short limited partnerships

As we complete our first anniversary, we want to thank our corporate and investor partners, and wish you all a healthy and happy new year! We look forward to initiating and continuing the discussions with allocators as we head into year-end.

MARKET UPDATE

The last three months through November 2021 have witnessed many of what we think are Leatherback’s themes play out. Over the past year, we have discussed at length that we think inflationary pressures are profound and have greater permanence than what was being guided by the Federal Reserve. The Fed Chair has now decided to “retire” the term “transitory” when referring to the current inflation dynamic.

“I think it’s probably a good time to retire that word [transitory] and try to explain more clearly what we mean” – Jerome Powell, November 29, 2021

Supply chain problems are still an overhang, with an unclear picture of what the future will bring for the broad range of industries being impacted. We have noted what we thought could be a compression in profit margins given employment and cost pressures, and we are starting to see this take shape. We have talked about and seen oil and prices at the pump push higher than most Americans are comfortable with, and even policy coming out of Washington in an attempt to address the concern. Despite these headwinds, our last note pointed out the broad asset markets continued willingness to march on to higher and higher levels.

SO WHAT NOW?

The tape now finds itself having a difficult time making up its mind. One of the overarching questions of who the next Fed Chair would be has been answered. Now that Jerome Powell has been renominated for a second term, how policy will be implemented from here is the next driver of anxiety that markets are trying to sort through.

"The stock market, and risk assets broadly, have been supported for over a decade by the Fed's balance-sheet expansion. As we move into tapering and ultimately raising interest rates, it's turning into rougher waters for markets.4" – Jeffrey Gundlach

We now know after the December Federal Open Market Committee meeting that the Fed is very concerned about inflation prints and has already accelerated the taper schedule. The number of times they expect to raise interest rates over the next year or so has also ticked up. The questions now are what will happen given the capitulation on inflation and the grappling with the pace of the reduction of quantitative easing, and how and when will possible balance sheet runoff take place? Separately, the debt ceiling seems to be resolving itself with little fanfare. Finally, the latest variant has recently found itself in the news, and as we write this US Treasury yields, US equity markets and Oil are all playing a game of ping pong trying to figure out if and where new levels may land.

No matter how markets shake out, we think there are opportunities to explore, and we look forward to continuing our dialogue in the weeks and months ahead.