The Leatherback Long/Short Alternative Yield ETF (LBAY) (the “Fund”) net asset value (NAV) advanced by 10.16 % in October, compared to 8.10% for the S&P 500 Index. LBAY paid our twenty-third consecutive monthly distribution, at $.065 per share in October. This is a 2.56% SEC yield versus the S&P 500 Index dividend yield of approximately 1.71%, and the 10-Year US Treasury yield of 4.05%. Year to date as of October 31, 2022, NAV for the Fund has returned 16.13%, compared to a decline of 17.70% for the S&P 500 Index. NAV performance for the Fund to date since inception (November 16, 2020) has produced a 48.33% cumulative total return and a 22.33% annualized total return.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling (833) 417-0090. The gross expense ratio for the fund is 1.43%.

View LBAY standardized performance here.

The Fund’s NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the Fund was traded.

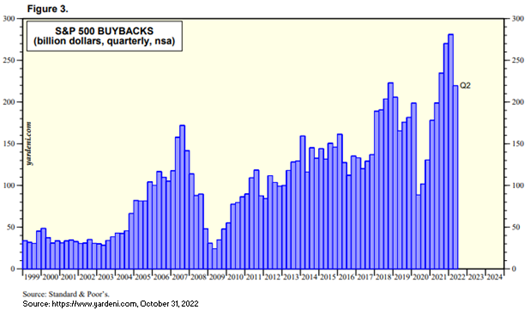

A key tenet to the Leatherback investment process is to identify company management teams that deploy capital in a prudent manner. Conversely, on the short side of the book we look for companies that misallocate capital. In the year 2022, poor allocators are seeing decisions come home to roost. There is a long list of companies who levered their balance sheets to repurchase shares of their own stock over the last several years. For many management teams, we think this was a method that was heavily reliant on near zero interest rates. As can be the case with the timing of capital deployment decisions like this near the top of a cycle, many of the shares repurchased were likely at frothy levels, rather than at levels that may be perceived as corrected or more attractive. We do not look to simply criticize the timing of purchases with the benefit of hindsight, but we do have to wonder: Has this large market participant disappeared for the remainder of this cycle?

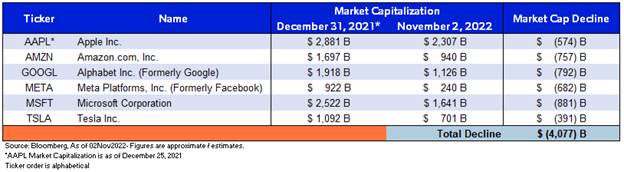

THE S&P FIVE (OR SIX)

In August of 2021, we were intrigued by the concentration of the big five constituents in the S&P 500 Index. We took the view that too many investors and passive managers were piled into this small group of names, which we thought in essence had turned into defining the entire market itself. We called this the Trillion Dollar Club, and thereafter a sixth member joined. 2022 has been a difficult year for these names, which are just recently beginning to slip and lead the US Stock Market lower. Take a look at the below table, which shows the billions of dollars in market capitalization decline in these six mega-cap growth companies:

The destruction of capital among these names this calendar year is remarkable with over $4 trillion in market capitalization vanishing. Our view is that passive investment vehicles tend to funnel flows into these larger market cap names, compounding the moves up over the years, and now back down in 2022. Interestingly, passive investment products have increased in acceptance over the years, which we think reflects current market participant sentiment. One segment of passive vehicles we find fascinating of late are the momentum trackers. With a quick peel back of the onion for one of these momentum tracker funds, we find the most recent holdings telling; we think large cap value defensive characteristics reflect the new momentum, replacing the growth leaders of the past few years.

PORTFOLIO UPDATE*3

We have been pleased with how our portfolio has performed thus far in 2022. Notably, in October we had winners on both the long and short side of the book. On the long side, positions in Exxon Mobil Corporation (XOM), Bunge Limited (BG) and Lancaster Colony Corporation (LANC) were the largest contributors to performance in October. Each of these names have a history of annual dividend increases and share buybacks. Interestingly, they are each up nicely on the year through October 31, 2022, far exceeding the S&P 500 Index performance with XOM up 86.72%, BG up 7.43% and LANC up 10.67% on a total return basis.

In October, our three largest detractors were short positions in Stifel Financial Corp. (SF), Lululemon Athletica Inc. (LULU) and Blackrock, Inc. (BLK) all of which we continue to maintain short. Additionally, we would like to highlight a short position in SVB Financial Group (SIVB) which declined by over 30% in October and has been one of our largest short winners in 2022. In our March 2022 commentary (“End Of An Expansion Era”) we laid out our high conviction short thesis in the name. We continue to maintain a short position in SIVB as we think it has further downside.

During the second half of 2022 we initiated a position in Intercontinental Exchange, Inc. (ICE). ICE attracts us as it maintains one of the largest commodity and financial product marketplaces globally providing market infrastructure, data services and technology solutions spanning a variety of asset classes. Importantly, we think ICE’s consolidated operating margin profile of 50% highlights the attractiveness of its businesses. Despite macro headwinds, the company recently reported what we view as strong metrics. It’s currently in the process of antitrust review with Black Knight, Inc., a mortgage technology acquisition, that we hope will remove overhang in the next several months as the company has suspended share repurchases while the acquisition is pending4.

View LBAY top 10 holdings here. Holdings are subject to change. Characteristics and metrics of the companies shown are for the underlying securities in the fund’s portfolio and do not represent or predict the performance of the fund. There is no guarantee that a company will pay or continually increase its dividend.

FINAL THOUGHTS

We hope our investor partners enjoy our monthly perspectives. We are finding many compelling ideas both long and short and we look forward to continuing our dialogue in the weeks and months ahead.