The Leatherback Long/Short Alternative Yield ETF (LBAY) (the “Fund”) net asset value (NAV) declined by 7.59% in May, compared to an advance of 0.43% for the S&P 500 Index. LBAY paid its thirtieth consecutive monthly distribution, at $0.075 per share in May. This is a 2.87% SEC yield versus the S&P 500 Index dividend yield of approximately 1.66%, and the 10-Year US Treasury yield of 3.646%. Year to date as of May 31, 2023, NAV for the Fund has declined 12.83%, compared to an advance of 9.65% for the S&P 500 Index. NAV performance for the Fund to date since inception (November 16, 2020) has produced a 36.27% cumulative total return and a 12.97% annualized total return.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling (833) 417-0090. The gross expense ratio for the fund is 1.32%.

View LBAY standardized performance here.

The Fund’s NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the Fund was traded.

THE RATE TIGHTENING IS REAL

We find it noteworthy that nominal interest rates are finally above the inflation rate, and real rates are now positive. Until recently, we suppose savers and users of credit were better off spending cash since there was a cost to not doing so. In essence, if you were to sit on cash there would be a negative impact as inflation exceeded the rate you could earn on that cash. Put simply, it could be more expensive in real terms to NOT spend. We think this caused the now-possibly entrenched mindset that prices would remain high, therefore causing consumers and investors to deploy cash now believing it may be even more expensive in the future. So, what does this mean? We think these brought-forward expenditures and investments have been a major driver of lofty goods, services, and risk asset prices. In our opinion, the recent interest rate paradigm provided the incentive to spend now rather than later and has been conflated as growth.

This brings us to today, where we find recent inflation rates are now below shorter-term interest rates. For the first time in quite some time, there is an actual cost of funds. The preference and ability to consume or invest currently may now be switching to a preference for future consumption and investment given the resumption of a cost to doing so. We do not believe it takes much of a leap when pondering the impact of what could be described as insatiable appetites for levels of debt and worries of delinquency rate increases. Now consider these two characteristics with a backdrop of interest rates that may continue the march higher. We wonder, will the “growth” mentioned above begin to show unsustainability during the back half of 2023 and into the year 2024?

THEN AND NOW, NOW AND THEN

The below visuals show what we think summarize consumer budget impacts given the hardships of inflation. Over the past ten years you can see the spike in credit card balances that has taken place. It is then difficult to ignore the near-simultaneous increase in interest rates3. In our opinion, this is not a good recipe.

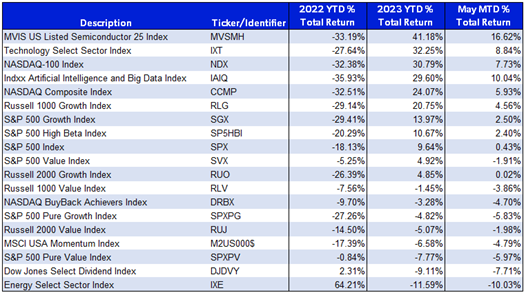

We leave you with one last chart showing what happened during 2022, this year to date, and during the month of May in equity markets4. We question whether this reflects a healthy market dynamic or is this basically a temporary revisiting of the pandemic market environment. Counterintuitively, as real rates have risen and debt levels continue their increase, long duration* equities have performed quite well. We think these two pain points of the true cost of funds will be felt and wonder how much longer the long duration equity rally may persist.

PORTFOLIO REVIEW5*

Our largest position continues to be Bunge Limited (BG), which maintains a $14B market capitalization and operates as a global agribusiness and food company; BG is a leading company in oilseed processing and supplier of specialty plant-based oils and fats. Notably, the company just announced its intention to acquire Viterra Limited, the global agribusiness of Glencore PLC in an $8B transaction that is a mix of cash and stock, and additionally will include the assumption of Viterra debt. We are very bullish on the deal as it transforms Bunge into a pure-play global agribusiness with highly complementary businesses and geographic footprints while diversifying BG’s footprint with increased grain handling and logistics assets. We are pleased to see that Glencore and key investors are retaining their ownership in the newly combined entity; also, credit rating agencies have placed the company’s credit profile under review for upgrade upon announcement of the deal. Additionally, the company will maintain its dividend per share and plans to execute a $2B stock buyback, equivalent to over 10% of the current market value as existing shareholders await the deal consummating. Pro forma with synergies, Bunge expects the combined entity to generate approximately $5.6B Adjusted EBITDA and roughly $3.2B in discretionary cash flow. We expect Bunge to be a core holding and for value to accrete higher over the medium term.

Next, we continue to be long medical device companies Zimmer Biomet Holdings, Inc. (ZBH) and Medtronic, PLC (MDT). We are pleased to see industry participants confirm the thesis we have maintained on the medical device space since coming out of COVID; our thesis was specifically that pent up demand was significant for the oligopolist replacement hip and knee industry, and medical devices generally, and these two companies would be beneficiaries.

“[Seniors are accessing services for] things that they might have pushed off a bit like knees and hips…We’re just seeing more services, which, again, we’re really happy to see that our seniors are accessing the care that they need.”6 - Tim Noel, CEO UnitedHealthcare Medicare & Retirement

One sector we maintain short exposure is in the real estate sector, with short positions in Equinix, Inc. (EQIX) and Prologis, Inc. (PLD).

"When we raise interest rates we think, and we usually are correct, that we're going to decimate the real estate market, both commercial and residential."7 – Alan Blinder, Former Federal Reserve Vice Chair

View LBAY top 10 holdings here. Holdings are subject to change. Characteristics and metrics of the companies shown are for the underlying securities in the fund’s portfolio and do not represent or predict the performance of the fund. There is no guarantee that a company will pay or continually increase its dividend.

FINAL THOUGHTS

We hope our investor partners enjoy our monthly perspectives. We are finding many compelling ideas both long and short and we look forward to continuing our dialogue in the weeks and months ahead.