The Leatherback Long/Short Alternative Yield ETF (LBAY) (the “Fund”) net asset value (NAV) declined by 6.36 % in September, compared to a decline of 9.21% for the S&P 500 Index. LBAY paid our twenty-second consecutive monthly distribution, at $.065 per share in September. This is a 2.64% SEC yield versus the S&P 500 Index dividend yield of approximately 1.85%, and the 10-Year US Treasury yield of 3.832%. Year to date as of September 30, 2022, NAV for the Fund has returned 5.42%, compared to a decline of 23.87% for the S&P 500 Index. NAV performance for the Fund to date since inception (November 16, 2020) has produced a 34.66% cumulative total return and a 17.24% annualized total return.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling (833) 417-0090. The gross expense ratio for the fund is 1.43%.

View LBAY standardized performance here.

The Fund’s NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the Fund was traded.

BEAR MARKET RALLY ENDS WITH A WHIMPER

Markets have been sliding lower after a nice summer rally. From the recent low in mid-June 2022 through mid-August the S&P 500 Index produced a total return of over 17%. Since then, the market has retraced all those gains and is resting near the lows of the year at the time of this writing. In our opinion, the hope of a Federal Reserve “pivot” (rate cuts in 2023) and soft landing drove the risk-on mid-summer bullish sentiment. Meanwhile, Chairman Jay Powell seems to have morphed into Paul Volcker over the last several months. Notably, the US Federal Reserve Board (the Fed) has hiked rates five times over that time span. In public appearances Chair Powell has repeatedly referenced Volcker when referencing inflation, recently stating that “we must keep at it until the job is done” invoking Volcker’s 2018 biography “Keeping At It”. Not surprisingly, as interest rates reset higher, stretched stock and bond valuations re-rated lower. We think this environment is ideal for long-short strategies.

SINGLE MANDATE

“Until inflation comes down a lot, the Fed is really a single mandate central bank.3” – Former Fed Vice Chair Richard Clarida

We questioned the concept of the potential fallacy of the Fed “dual mandate” in our insights almost a year ago to the day. We pointed to market and asset prices as a possible, if not probable, driver of much of the policy seen leading up to that time. The Fed seemed to indicate at the time that deflation was a concern, so policy was guided in the direction of lifting prices above the stated 2% target rate of inflation.

“I would say our policy is well positioned to manage a range of plausible outcomes — I do think it’s time to taper, and I don’t think it’s time to raise rates. It would be premature to do so at a time when we are far below the level of jobs we had in 2020.4” – Jerome Powell in October 2021

This tone has clearly changed, as the messaging is being conveyed loud and clear: prices are too high and must come down. This seems to be the only mandate of the traditional two that the Fed is focusing on, no matter how much market participants may not want to believe it. Interestingly, bullish market participants search for a new narrative to justify holding risk assets. A year ago, inflation was transitory. This past summer the Fed pivot drove a bear market rally. We are now being introduced to a “stepping down” in interest rates, which is the equivalent of smaller incremental interest rate increases.

“The time is now to start planning for stepping down.5” - San Francisco Fed President Mary Daly

2000 vs 2022

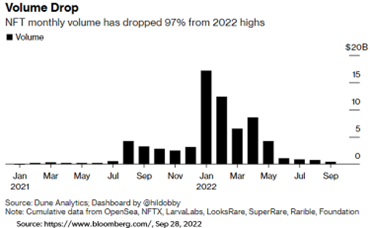

The founders of Leatherback both entered the investment management industry near the end of the dot-com bubble. The current investing climate seems to rhyme with the 2000 to 2002 period. It has been quite nostalgic to listen to and witness this generation learn about investing. When we first entered the investment management industry in 1999, the world was captivated by technology stocks. At the time, many were dabbling in the shares of internet companies, and were discussing reaping paper wealth. There was a fascination with the internet and any stock with a “dot-com” at the end of it. In 2000 it all crashed, and by late spring of that year, we do not recall anyone boasting about any realized gains. Growth stocks were walloped, and growth equities declined for a couple of years thereafter. History seems to be repeating; over the last two years, we have heard quite a bit about metaverse companies, social media, cryptocurrencies, and non-fungible-tokens (NFTs). A recent article pointed out NFTs specifically, showing how recent policy is impacting speculative assets6:

In the year 2022 through the end of September 30, total returns have exhibited pain. Growth equities have declined significantly with the S&P Growth Index7 and NASDAQ Composite Index7 falling over 30% each. The Ball Metaverse Index7 declined more than 50% and the BUZZ NextGen AI US Sentiment Leaders Index7 has tumbled 45%. AMC Entertainment Holdings, Inc. stock – a poster child stock for the fintwit crowd- is now down more than 58% year to date through the end of the third quarter.

Anecdotally, I recently had a twenty-two-year-old nephew of mine ask me about Series I Savings Bonds (I Bonds) and Certificates of Deposit (CDs). Previous conversations had typically centered around NFTs, the metaverse or crypto. He no longer has any interest in those topics as he now finds himself with both realized and unrealized losses. From a bigger picture, the market sentiment seems very similar to 2000 with risk appetites vanishing. While we are not investing in CDs, we think 2000 marked an ideal entry point for value equities.

PORTFOLIO UPDATE*8

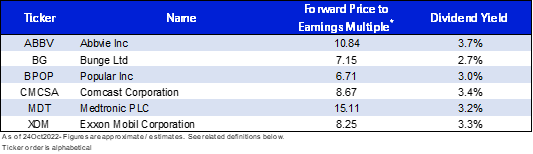

As we canvas the opportunity set for investment ideas, we observe many companies with multiples at what we view is a discount to the overall market that maintain robust profit margins. As we deploy capital, we expect to be opportunistic in upgrading our long portfolio adding to our highest-conviction ideas. In our opinion, our long book has many examples of companies already exhibiting attractive valuations. Below we show 2022 Forward Price to Earnings (P/E) multiples and Dividend Yield of some of our core long positions:

We believe larger cap companies with multiple divisions will be exploring strategic alternatives to unlock value. Recently, we initiated a position in General Electric Co (GE). GE has been in decline for almost two decades and was formerly an iconic American company that at one time held the title of the largest market capitalization in the US stock market. GE plans to split itself into three companies, with GE HealthCare anticipated to be spun-off in early 2023. The company expects this to be followed by GE Vernova, its portfolio of energy businesses, in early 2024. Following the planned spin-offs, GE Aerospace will remain as an aviation-focused company9. We think that as GE is re-sized and singularly purposed the new companies will have highly motivated management teams that will be able to invest and deploy capital without the limitations of its parent company distractions. We expect to be long-term holders of GE as it re-creates and re-brands itself over the next several years.

"There are plenty of reasons why a company might choose to unload or otherwise separate itself from the fortunes of the business to be spun-off. There is really only one reason to pay attention when they do; you can make a pile of money investing in spin-offs." - Joel Greenblatt

"Spin-offs of divisions or parts of companies into separate, freestanding entities…often result in astoundingly lucrative investments” - Peter Lynch

Conversely, there continues to be many securities that we think are ideal short candidates given what we view as current overvaluation. On the short side of the book, we have been increasing our exposure to the “size” factor as we believe flows out of expensive large cap stocks may deflate rich multiples of mega cap stocks; we also continue to be negative on the semiconductor space, due to concerns over international trade relations and the overall economic environment. We think semiconductor stocks tend to perform poorly in recessionary environments. We currently maintain short positions in Nvidia Corp (NVDA) and Broadcom Inc (AVGO), which boast market capitalizations of over $300B and $175B respectively and provide what we think is exposure to the global economy.

View LBAY top 10 holdings here. Holdings are subject to change. Characteristics and metrics of the companies shown are for the underlying securities in the fund’s portfolio and do not represent or predict the performance of the fund. There is no guarantee that a company will pay or continually increase its dividend.

FINAL THOUGHTS

We hope our investor partners enjoy our monthly perspectives. We are finding many compelling ideas both long and short and we look forward to continuing our dialogue in the weeks and months ahead.